Procedure for calculation and payment of excise tax

The day on which the excise goods are sent (handover) to the recipient is the date on which the taxable transactions related to the excise goods are carried out.

In the event that the pledged excise goods are handed over by the pledger, the date of transfer of the property right to the pledged item is the date of realization of the transaction for the pledger.

Excise tax rates are determined in absolute amount (fixed) based on the tax base for excise goods, expressed in kind.

Excise tax rates are determined in percentages (ad valor) on manufactured excisable goods, excise tax and value-added tax excluded value of realized excise goods is the taxable base.

Adjustments to the income from the sale of goods (works, services) in the cases stipulated by the tax legislation shall be made in the tax period in which the specified cases occurred.

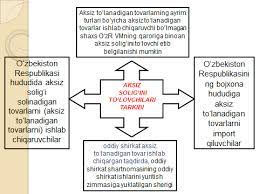

Documents confirming the export of excise goods are as follows:

A contract for the delivery of exportable excise goods.

Customs cargo declaration with the mark of the customs authority that performs the export of goods.

Documents to be attached to goods with a mark confirming that the goods have been sent to the designated country by the customs authority located at the transfer point at the customs border of the Republic of Uzbekistan.

When receiving excise goods or importing them to the customs territory of the Republic of Uzbekistan, if these goods were subsequently used as raw materials for the production of excise goods, the amount of excise tax paid in the territory of the Republic of Uzbekistan is deducted.

Suppliers of excisable goods (raw materials) must specify the amount of excise tax on these goods (raw materials) in the invoice. If the amount of excise tax on excise goods (raw materials) received is not specified in the invoice, this amount of excise tax is not deducted.

The discount is made in relation to the amount of excise tax specified in the invoice or customs cargo declaration, determined based on the volume of excise goods (raw materials) corresponding to the volume of excise goods sold during the tax period.

Excisable goods made of raw materials and materials for processing are also used on the condition that the owner of the raw materials and materials subject to processing confirms that he has paid the excise tax.

The tax period is:

For micro-firms and small enterprises - a quarter of a year.

For taxpayers not included in micro-enterprises and small enterprises — one month.

Calculation of excise tax to the state tax service authorities at the place of tax registration:

By micro-enterprises and small enterprises that are excise tax payers - every quarter of the year no later than the 25th day of the month following the tax period.

By taxpayers who are not included in the category of micro-firms and small enterprises - submitted monthly no later than the 25th day of the month following the tax period.

The amount of excise tax calculated in accordance with the tax legislation is paid to the budget in the following terms:

No later than the 13th day of the current month — for the first ten days of the current month.

No later than the 23rd day of the current month — for the second ten days of the current month.

No later than the 3rd day of the next month — for the remaining days of the reporting month.

The date of customs clearance of imported excise goods is the date of transaction.

Payment of excise tax on imported goods is carried out within the terms established by the customs legislation.

Excise duty on imported excise goods that must be stamped with excise stamps is paid before receipt of excise stamps.

Tobacco products and alcoholic beverages produced in the territory of the Republic of Uzbekistan, as well as imported into its customs territory, must be marked with excise stamps in accordance with the procedure established by the Cabinet of Ministers of the Republic of Uzbekistan.

Brief conclusions

In conclusion, it can be said that according to the taxation system, the excise tax is calculated from indirect taxes and added to the tariff of the price of goods, which directly affects the increase in the price of consumer goods. Excise duty is a type of indirect tax on goods, which is added to the price of a certain limited type and group of goods, unlike value added tax. In ancient times, excise taxes made a significant contribution to the formation of budget revenues of all countries. Because through excise taxes, it was possible to collect financial resources necessary for state needs through a quick and simple taxation mechanism.

In the tax system of the Republic of Uzbekistan, excise duties play a key role in the formation of state financial resources. The need to levy excise tax on certain goods is necessary for the regulation of certain economic and social processes by the state, in addition to using them as an additional source of income for the state budget.

Indirect taxes, in particular, excise tax, are one of the main taxes in the formation of state budget revenues, and the highest tax revenues in the structure of state budget revenues are made from these taxes.

Review and discussion questions

1. What does the concept of excise mean?

2. When was the excise tax introduced in the Republic of Uzbekistan?

3. Who are the excise tax payers?

4. What is included in the object of excise tax?

5. What are the tax credits for excise tax?

6. What are the excise tax rates and calculation procedure?

7. In what terms is the amount of excise tax paid to the budget?

8. What is the procedure for transferring excise tax to the republic budget?

9. What is the procedure for reflecting excise tax in the customs cargo declaration?

Basic literature

1. Islam Karimov. 2012 will be a year that will raise the development of our country to a new level. T.: Uzbekistan, 2012. - 36 p.

2. I.A. Karimov. The concept of further deepening of democratic reforms and development of civil society in our country. Report at the joint meeting of the Legislative Chamber and the Senate of the Oliy Majlis of the Republic of Uzbekistan. T.: Uzbekistan, 2010. - 56 p.

3. Study guide for the study of the speech of the President of the Republic of Uzbekistan I.A. Karimov on the topic "2011 will be the year that will raise the development of our country to a new level" at the meeting of the Cabinet of Ministers of the Republic of Uzbekistan, dedicated to the results of socio-economic development of our country in 2012 and the most important priorities for 2012. - Tashkent: NMIU "Teacher". - 2012. - 382 p.

4. State program of the President of the Republic of Uzbekistan No. PQ-1717 "Strong family year". February 2012, 27.

5. Tax Code of the Republic of Uzbekistan. Collection of legal documents of the Republic of Uzbekistan, January 2012.

6. Nikulkina IV Obshchaya teoriya nalogooblozheniya: Uchebnoe posobie - M.: Eksmo, 2010. - 145-156 p.

7. Vahobov A., Jo'raev A. Taxes and taxation. Textbook - T:. Sharq, 2009. - 408-418 pages.

8. Tukhliev BK, Yusupov O.A., Agzamov A.T, Tokhsanov QN Taxes and taxation: Study guide. - T.: 2007.-228-260 p.

9. Yahyoev Q. "Taxation Theory and Practice" Textbook -T.: Science and Technology Center, 2003. Pages 16-45.